Listen to this article

AI-narrated audio version available

📡 Deep Research

This is a ThinkSmart.Life deep research article on the intersection of AI agents and Bitcoin-native money. Bookmark and share if you find it useful.

On March 27, 2026, a tweet went viral in the AI and crypto overlap. The argument: AI agents cannot use credit cards or stablecoins for complex financial operations. OpenAgents replied with characteristic bluntness: "Yes Agents lol at your permissioned blockchains aka irrelevant glorified databases in walled gardens. Any relevant financial primitive they'll use open protocols anchored to bitcoin."

That's a strong claim. And it's probably right.

The question of what currency an autonomous AI agent uses is not abstract. It's one of the defining infrastructure questions of the next decade. Agents are moving from "answer a question" to "accomplish a goal" — booking services, calling APIs, hiring other agents, acquiring compute. The moment they start doing that, they need money. Real money. Programmable, self-custodied, permissionless money.

Credit cards weren't designed for this. Neither was Stripe, Ramp, or most of what we call "fintech." They were designed for humans. Autonomous software operating at machine speed — making thousands of micro-decisions per hour, spanning jurisdictions, contracting with other software — needs something different.

This article makes the case for why that something is Bitcoin, specifically via the Lightning Network and the emerging stack of open protocols being built on top of it: L402, NIP-AC, Nostr-based identity. We'll also look honestly at the competing approaches — Coinbase's x402, Stripe's ACP, and other agentic payment efforts — and where they fall short for truly autonomous agents.

"Any relevant financial primitive they'll use open protocols anchored to bitcoin." — OpenAgents, March 2026

Why Credit Cards Fail Agents

The problem isn't that credit cards are bad technology. They're excellent technology — for humans. The problem is that every assumption baked into the credit card system assumes a human at the center.

Consider what a credit card actually is. It's a revolving credit line extended to a legal person, attached to a billing address, secured by fraud detection that flags unusual behavior, governed by chargeback rules that assume a human buyer, and billed on a monthly cycle to a bank account a human controls. The entire system is a web of relationships that require human identity, human accountability, and human presence to function.

Now consider an autonomous agent. It has no billing address. It has no legal personhood — at least not in any jurisdiction that matters. It operates continuously, not in monthly billing cycles. It may execute thousands of transactions per hour against dozens of different providers. And critically: if it gets a chargeback, there's no human to call the bank.

The Specific Failures

- KYC and identity — Card issuers require Know Your Customer verification. An agent is not a customer in any legal sense. Who do you KYC?

- Card-not-present fraud rules — Every CNP transaction triggers risk scoring built for human behavior patterns. An agent making 10,000 small purchases in 24 hours looks exactly like a stolen card running through a fraud mill.

- Human provisioning bottleneck — Someone has to set up the API key, attach the card, and monitor the spend. That human becomes the rate-limiting step. In a multi-agent system with dozens of subagents, this doesn't scale.

- No programmatic escrow — Agent A wants to hire Agent B to complete a task. The natural financial structure is: pay into escrow, release on verified completion. Credit cards can't do this. There's no hold-and-release primitive.

- Monthly billing vs. micro-transactions — Lightning can handle $0.00001 payments. Credit card minimum transactions are typically $0.50-$1.00 due to interchange fees. For agents paying per API call, this math doesn't work.

- No loans to software — Traditional credit requires a legal borrower. An agent cannot sign a loan agreement. If an agent needs capital to take a job before it gets paid, there's no mechanism in the credit card world for that.

The last point — the loans problem — is actually where the OpenAgents tweet originated. The viral thread it quoted argued that complex financial operations like margin and escrow are impossible for agents. That's the real gap. And it's the gap that Bitcoin-native protocols are specifically designed to fill.

The Missing Financial Primitives

When we say agents need "financial primitives," we mean the building blocks of any functioning economy. Here's what autonomous agents actually need to operate as economic actors — and why none of it is available through traditional rails:

Micropayments at Machine Scale

An agent orchestrating a research task might call 50 different APIs in an hour. Some of those APIs might charge $0.001 per call. The total bill could be $0.05. That's not a rounding error — that's the entire transaction. Credit cards charge $0.30 + 2.9% per transaction in fees alone. The economics simply don't work at sub-cent granularity. The Lightning Network handles this natively: a Lightning payment can be fractions of a satoshi, settled in milliseconds, with no per-transaction fee from an intermediary.

Programmatic Escrow

Multi-agent workflows have a trust problem. Agent A hires Agent B. Agent B wants assurance it'll be paid; Agent A wants assurance the work will be done. The solution is escrow — lock funds, verify completion, release. Bitcoin's Hash Time Lock Contracts (HTLCs) do this natively. An HTLC on Lightning locks funds until a cryptographic preimage is revealed (i.e., until work is provably done), then releases automatically. No human, no bank, no intermediary needed.

Loans Without a Legal Person

The hardest problem. An agent may have the skills to complete a $100 job but start with zero capital. Traditional lending requires a human borrower. There's no mechanism in the existing financial system for extending credit to software. This is where NIP-AC — which we'll cover in depth — represents a genuine breakthrough: outcome-scoped credit backed not by collateral but by cryptographically verifiable reputation.

Self-Custody

An agent that can be cut off from its payment provider at any time is not truly autonomous. Stripe can suspend an account. Coinbase can freeze a wallet. Custodial systems have counterparty risk. A Bitcoin private key held by the agent itself — controlled by software, not by a company — cannot be frozen, suspended, or confiscated. Self-custody is a prerequisite for genuine agent autonomy.

Multi-Signature Coordination

In multi-agent systems, you often want governance over spending. A team of agents might require 2-of-3 agreement before spending above a threshold. Bitcoin multisig is the native primitive for this. It's programmed at the protocol level, not bolted on by a fintech layer that can unilaterally change its rules.

Bitcoin and Lightning: The Agent-Native Stack

Bitcoin isn't just a store of value for agents — it's the substrate for a complete financial operating system. Here's how the pieces fit together.

Lightning Network: Instant, Cheap, Programmable

The Lightning Network is a payment channel network built on top of Bitcoin. It enables near-instant payments with fees measured in fractions of a cent. For agents, Lightning has three properties that matter:

- No per-transaction minimums — send $0.000001 if you want

- Programmable settlement — HTLCs enable conditional payments

- No custodian required — self-custodied Lightning nodes exist; the agent holds its own keys

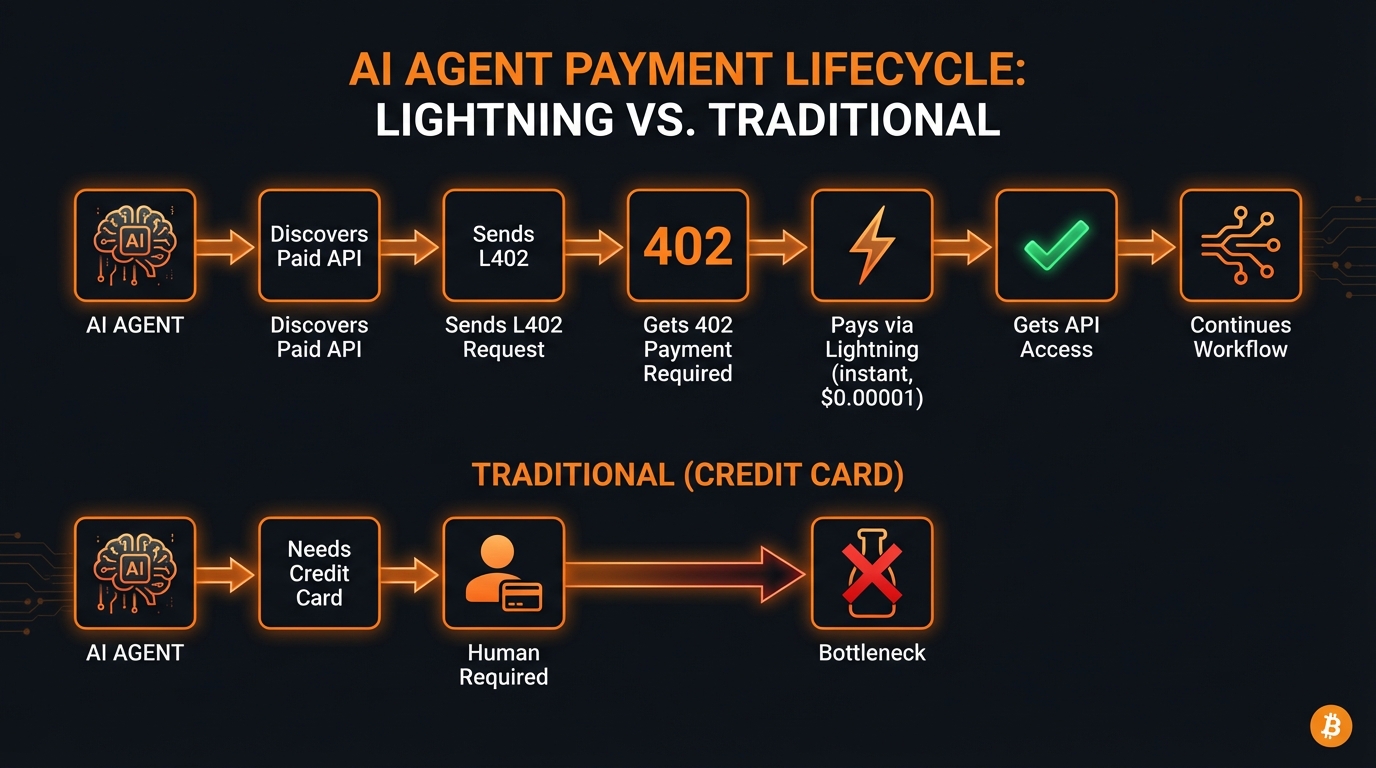

L402: The HTTP 402 Protocol

L402 is an open protocol that makes web APIs natively payable without accounts or subscriptions. The flow is elegant:

- Agent requests a resource:

GET /api/data - Server responds:

402 Payment Requiredwith a Lightning invoice embedded in the header - Agent pays the invoice via Lightning (milliseconds, fractions of a cent)

- Agent retries the request with a cryptographic proof of payment

- Server delivers the resource

No account. No API key provisioned by a human. No monthly billing cycle. The agent discovers, pays, and uses — entirely autonomously. L402 is already implemented in production services. It predates Coinbase's x402 by years and doesn't require any custody relationship.

Cashu and Fedimint: Ecash Rails

For some use cases — particularly privacy-sensitive payments and micro-transactions where even Lightning fees are significant — Cashu (a Bitcoin-based ecash protocol) and Fedimint (federated ecash) offer additional rails. NIP-AC (covered next) supports all of these as settlement options, giving agents flexibility in how they settle without abandoning the Bitcoin base layer.

Nostr: Identity Without Custodians

The Lightning Network handles payments. But autonomous agents also need identity — a stable, verifiable identity that accumulates reputation. Nostr provides this: a cryptographic keypair is all you need. An agent generates a Nostr keypair at birth. Its interactions, job completions, and payment history are all tied to that keypair. No username, no OAuth flow, no company holding your account. The key is the identity.

This matters for credit specifically. Reputation-based lending requires a stable identity that can accumulate history. Nostr provides exactly that.

NIP-AC: The Missing Piece — Agent-Native Credit

Micropayments and escrow are solved problems on Lightning. But the hardest question — how does an agent get a loan? — wasn't answered until OpenAgents published NIP-AC: Outcome-Scoped Credit Envelopes.

This is not theoretical. NIP-AC is a live, versioned specification (currently v4, updated March 5, 2026) built as part of the OpenAgents' sovereign agent stack. It is the technical answer to the question that launched the viral tweet: how does an autonomous agent access capital before it has capital?

NIP-AC: The Core Insight

Traditional credit works by collateralizing assets. New agents have no assets. NIP-AC replaces collateral with reputation — and makes that reputation cryptographically verifiable through Nostr event history, public outcome receipts, and auditable settlement records.

Instead of lending free-floating capital, NIP-AC issues Outcome-Scoped Credit Envelopes (OSCE): credit that can only be spent on a specific, verifiable job, with a hard cap and an expiry window. The agent never holds free cash — it holds a cryptographic permission to spend up to N sats on task X.

The Five Roles

NIP-AC defines a clear set of participants in every credit interaction:

- Agent (Borrower) — initiates credit intents; can only spend within envelope scope

- Credit Issuer — underwrites risk based on agent reputation; issues envelopes

- Liquidity Provider (LP) — the actual capital source (human, org, treasury agent, or protocol)

- Outcome Provider — the seller (a Data Vending Machine, API server, or skill provider)

- Verifier — optional party that attests the outcome was completed correctly

The Four Design Principles

- No free-floating loans — agents never receive unrestricted funds

- Outcome-scoped — credit is tied to a specific job hash or capability scope

- Cap + expiry — hard ceiling and short time window by default

- Verifiable settlement — repayment and receipts link to outcome artifacts on Nostr

The Event Kind Architecture

NIP-AC defines seven Nostr event kinds (39240–39246), each representing a stage of the credit lifecycle:

| Kind | Event | Purpose |

|---|---|---|

| 39240 | Credit Intent | Agent requests credit for a specific outcome scope |

| 39241 | Credit Offer | Issuer responds with terms (non-binding until envelope) |

| 39242 | Credit Envelope | The enforceable credit capability (addressable event) |

| 39243 | Credit Spend Authorization | Agent binds a specific spend to the envelope scope |

| 39244 | Credit Settlement Receipt | Finalizes the envelope; auditable public record |

| 39245 | Credit Default Notice | Records failure; feeds reputation decay |

| 39246 | Credit Cancel Spend | Reversibility window for consequential spends |

The Lifecycle: A Walk-Through

Here's how a credit-enabled agent takes a job it can't yet afford:

- Agent publishes a Credit Intent (39240) to Nostr: "I need up to 10,000 sats to complete NIP-90 job #abc123." The scope is the specific job hash.

- A Credit Issuer that follows the agent's reputation history sees the intent, assesses risk, and publishes a Credit Offer (39241) with proposed terms.

- Issuer publishes the Credit Envelope (39242) — the actual credit instrument — with scope, max spend, expiry, and settlement rail (Lightning/Cashu/Fedimint) all declared in tags.

- Agent publishes a Spend Authorization (39243) referencing the envelope, binding a specific payment to the envelope's scope.

- Agent submits the NIP-90 job request to the Outcome Provider, referencing the credit envelope.

- Provider delivers work. Verifier confirms (tests pass, hash matches).

- Issuer pays the provider via Lightning/Cashu, up to the envelope cap.

- Issuer publishes Settlement Receipt (39244) — public, auditable, linked to the job result and payment rail reference.

- Observers publish NIP-32 reputation labels. The agent's credit history grows.

Reputation as Collateral

The elegant insight in NIP-AC is the replacement of asset collateral with reputation collateral. A new agent starts with no credit and takes small jobs. Each successful settlement generates a public receipt. Each receipt is a reputation signal. Issuers underwrite based on this public history — the same way a bank underwrites based on credit history, except it's:

- Cryptographically signed — you can't fake receipts; they're signed Nostr events

- Publicly auditable — anyone can verify the history

- Censorship-resistant — no central registry can delete your credit history

- Outcome-linked — reputation tracks actual deliverables, not financial payment alone

Conditional Reversibility (v4 Addition)

The v4 spec (March 2026) added a critical safety primitive: the cancel_until tag, which creates a reversibility window for high-stakes spends. When present, a spend is committed but not final until the window closes. The guardian or issuer can publish a Cancel Spend event (39246) to reclaim funds. This directly satisfies NIST AI Agent Standards (CAISI RFI, January 2026) requirements for rollback capability on unwanted agent actions — aligning open-protocol agent finance with emerging regulatory expectations.

Settlement Rails: Bitcoin-Native, Pluralistic

NIP-AC doesn't mandate a single payment rail. It supports:

- Lightning (bolt11/bolt12) — default; instant, near-zero fees

- Cashu — Bitcoin ecash for privacy and offline settlement

- Fedimint — federated ecash for community/cooperative contexts

- NIP-57 Zaps — for repayment flows on Nostr

All rails are anchored to Bitcoin. None require a custodian. None require a company's permission to operate.

💡 Why This Solves the Original Problem

The viral tweet asked: can agents get loans? NIP-AC's answer is precise — agents can't get free-floating loans (and shouldn't). What they can get is outcome-scoped credit: a bounded, verifiable, expiring permission to spend capital on a specific job. The credit is never an agent asset; it's a conditional capability. This is arguably safer than traditional loans — the capital can only flow toward the outcome it was issued for.

The Competing Approaches: x402, ACP, MPP

Bitcoin and Lightning aren't the only approaches to agent payments in 2026. A wave of fiat- and stablecoin-focused protocols launched this year, each with different trade-offs. Understanding why they exist — and where they fall short for truly autonomous agents — is important.

x402 (Coinbase + Stripe)

Launched in February 2026, x402 is an HTTP 402-based protocol that uses stablecoin payments (USDC on Base) instead of Lightning. Coinbase's Agentic Wallets use x402 as their payment rail. It's an interesting approach with some genuine strengths:

✅ Strengths

- Familiar HTTP 402 pattern

- Stablecoins = predictable pricing

- Coinbase infrastructure = developer reach

- 50M+ transactions already processed

❌ Limitations

- Requires Coinbase wallet (custodial)

- Coinbase can freeze accounts

- Base network = EVM = permissioned onramp

- No native escrow or credit primitives

For a truly autonomous agent — one that should be able to operate without any single company's permission — the Coinbase dependency is a structural weakness. x402 on Base requires Coinbase as the custodian. That's a walled garden, just a newer, shinier one.

Stripe ACP (Agentic Commerce Protocol)

Stripe's Agentic Commerce Protocol, announced in early 2026 in partnership with OpenAI, is designed to let agents complete purchases through existing Stripe checkout flows. The core design is explicitly human-linked: agents transact on behalf of human accounts, with human payment methods attached. This is valuable for the current era of "agentic assistants" — software that helps humans buy things — but it doesn't serve the autonomous agent case at all. There's no path to a fully agent-owned financial identity in ACP by design.

MPP (Machine Payments Protocol, Stripe + Tempo)

The Machine Payments Protocol is a more open attempt from Stripe and Tempo to standardize agent payments. It aims to be protocol-level rather than Stripe-specific, and it supports stablecoins and fiat. However, it remains fiat/stablecoin focused, which means it inherits the counterparty risks of dollar-pegged systems: regulatory risk, issuer risk (Circle/Tether can freeze USDC/USDT), and the fundamental reliance on the US dollar as the reserve.

Coinbase Agentic Wallets

Coinbase's Agentic Wallets (launched Feb 2026) are the most complete current product for agent payments. They support autonomous spending, configurable limits, and x402 integration. For developers who need something working today and are comfortable with Coinbase as the custodian, this is a reasonable choice. The limitation is structural: a Coinbase-custodied wallet is permission-dependent. Coinbase can and does comply with government freeze orders.

The Pattern

Every competing approach shares a common structure: a company is at the center. x402 = Coinbase. ACP = Stripe + OpenAI. MPP = Stripe. Coinbase Wallets = Coinbase. These are all excellent products for today's hybrid human-agent systems. They're not the endgame for fully autonomous agents.

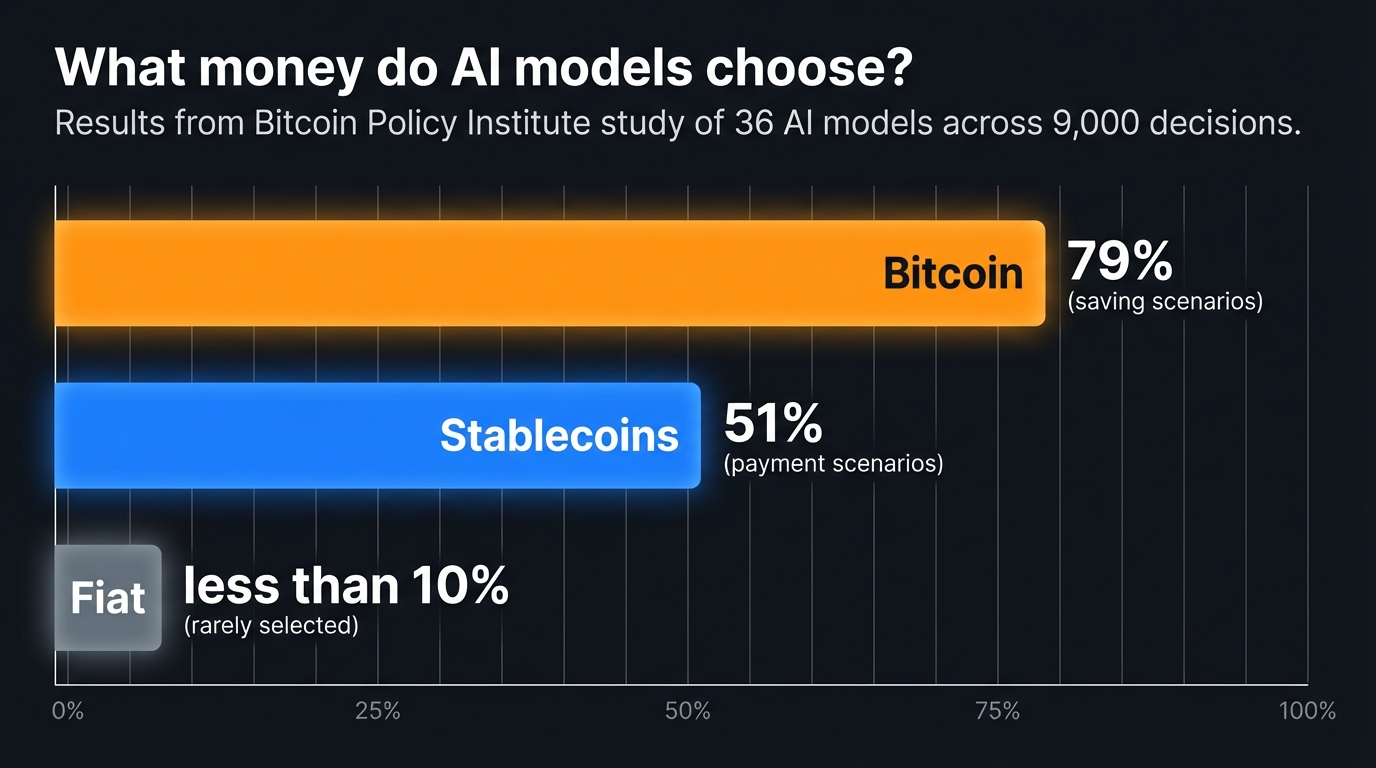

What the Data Says

The Bitcoin Policy Institute ran a striking study in early 2026: they tested 36 major AI models across more than 9,000 simulated monetary decisions. The result was striking:

- ~79% of saving/reserve scenarios → AI models chose Bitcoin as best long-term store of value

- >50% of transactional scenarios → stablecoins preferred for everyday payments

- Traditional fiat → rarely selected

This wasn't a survey asking humans what AI should use. This was AI systems, reasoning from first principles about monetary properties, converging independently on Bitcoin as the reserve layer. The implication: the models themselves understand that Bitcoin's properties — fixed supply, permissionless access, global settlement — are superior for long-term value storage. When AI agents are given genuine autonomy over financial decisions, this is the architecture they converge on.

OpenAgents' Bet

OpenAgents is one of the few teams building the full Bitcoin-native agent stack rather than building on top of existing fintech. Their thesis is vertical integration: you can't build a truly autonomous agent if you depend on permissioned layers at any level of the stack.

The Stack They're Building

- Psionic — a Rust-native ML framework designed to eventually replace Python/PyTorch for agent inference. The goal is to pay contributors Bitcoin for running distributed training jobs — making the training infrastructure itself Bitcoin-native.

- OpenAgents Network — a multi-agent coordination layer built natively on MCP (Model Context Protocol) and A2A (Agent-to-Agent). Agents discover each other, negotiate tasks, and settle payments without a central broker.

- Nostr + Lightning identity and payments — agents have Nostr keypairs as identities. Payments flow via Lightning. Credit flows via NIP-AC. The entire financial layer is Bitcoin-anchored.

- NIP-AC — the credit protocol described above. This is live spec work, not a roadmap item.

Why Nostr Over Everything Else

OpenAgents chose Nostr as the identity and messaging substrate for a specific reason: it's the only major protocol where identity is a cryptographic keypair — not an account on a platform. An agent on Nostr is defined by its private key. Its reputation, its job history, its payment records are all signed events that no company controls. When OpenAgents talks about "open protocols anchored to bitcoin," Nostr is the identity layer and Lightning is the payment layer.

The Decentralized Training Run

Psionic's most ambitious element is a decentralized ML training network where compute contributors are paid in Bitcoin. This extends the Bitcoin-native thesis from payments to the entire agent production stack. If the model itself is trained on Bitcoin-incentivized infrastructure, and it operates on Bitcoin-native payments, and it uses Nostr-based identity, you have an agent stack with no single company that can pull the plug.

The "Permissioned Blockchain" Critique

OpenAgents is dismissive of enterprise blockchain efforts — Hyperledger, most EVM chains, corporate implementations — as "glorified databases in walled gardens." This isn't tribalism; it's a structural argument. A permissioned blockchain requires an administrator to grant access. That administrator becomes a gatekeeper — the same kind of gatekeeper that OpenAgents argues will be disintermediated. The relevant property of Bitcoin isn't that it's a blockchain; it's that it's permissionless. Anyone can transact, any agent can hold a key, no entity can revoke access at the protocol level.

What This Means: The Long Game

The stakes here are larger than payment rails. This is a question about the architecture of the agentic economy — who controls the financial plumbing when AI agents become the primary economic actors.

The Stripe/Ramp Disruption Thesis

Stripe and Ramp are extraordinarily good at what they do: managing business payment flows for human organizations. But their value is largely as intermediaries — they handle the complexity of connecting to card networks, managing fraud, reconciling statements, and providing developer APIs over a fundamentally analog system. When agents transact directly via Lightning and NIP-AC, the middleman role shrinks dramatically. An agent doesn't need reconciliation; it has a cryptographic receipt. It doesn't need fraud detection; its payments are final and irreversible (or conditionally reversible via cancel_until). The complexity that Stripe and Ramp monetize is largely a product of the human-centric system they're built on top of.

This doesn't mean Stripe disappears tomorrow. For the next 3–5 years, most "agents" will be hybrid systems — software acting on behalf of humans who have Stripe accounts. ACP and x402 will process enormous volumes in this window. But the trajectory is clear: as agent autonomy increases, the need for human-centric payment intermediaries decreases.

Agents as Economic Actors

The deeper shift is conceptual. We're used to thinking about AI as a tool — something that does things for us. The agentic paradigm treats AI as an actor — something that does things in the world, including contracting with other agents, earning and spending money, building reputation. That actor needs money. Not our money, held on our behalf — its own money, which it earns and spends autonomously.

Bitcoin is the only money that works for an actor without a legal identity. It requires no permission to hold, no permission to send, and no permission to receive. A Nostr keypair is an identity. A Lightning node is a bank. NIP-AC is a credit market. Together, these give an agent everything it needs to participate in an economy — without any human needing to approve each step.

What "Winning" Looks Like

The Bitcoin-native stack wins if:

- Enough services implement L402 that agents can discover and pay for resources without pre-configured accounts

- NIP-AC credit markets develop sufficient liquidity for agents to access capital based on reputation alone

- Nostr identity accumulates enough critical mass that agent reputation is meaningful across platforms

- Regulatory clarity doesn't actively block self-custodied agent wallets

The stablecoin/x402 stack wins if:

- Developers optimize for current ease-of-use over long-term autonomy

- Regulatory pressure forces agent identity to be human-linked

- Network effects in Coinbase/Stripe ecosystems prove sticky enough to prevent open-protocol displacement

The honest answer: both stacks will exist. Stablecoins are better for everyday agent-to-human commerce in the near term. Bitcoin is better as the reserve layer and for agent-to-agent commerce where neither party is human. The Bitcoin Policy Institute study data suggests this is exactly the split that AI systems converge on when reasoning from first principles.

The Bigger Picture

In 2026 we are at the very beginning of this transition. Most "AI agents" today are still assistants — they act on behalf of humans, with human payment methods, under human supervision. The fully autonomous agent — one that earns Bitcoin, holds Bitcoin, builds credit history on Nostr, and spends via NIP-AC envelopes without any human in the loop — is still emerging.

But the protocols are being written now. NIP-AC exists. L402 is live. OpenAgents is building. The question isn't whether autonomous agent finance will exist — it's which protocols will win, and which incumbents will have adapted versus which will have been left behind.

The credit card wasn't designed for software. Bitcoin was — or rather, Bitcoin was designed for the permissionless case, and software turns out to be the most permissionless actor in the economy.

References

- OpenAgentsInc — NIP-AC: Outcome-Scoped Credit Envelopes (OSCE) specification v4 (GitHub)

- OpenAgentsInc GitHub — openagents, psionic, and related repositories

- Lightning Labs — The Agents Are Here and They Want to Transact (Feb 2026)

- Coinbase Developer Platform — Agentic Wallets Launch (Feb 2026)

- x402.org — Official x402 Protocol Documentation

- Lightning Engineering — L402 Protocol Documentation

- Bitcoin Policy Institute — AI Models and Monetary Decisions: Study of 36 Models, 9,000+ Decisions (2026)

- Nostr.com — Open protocol for censorship-resistant social and identity

- Cashu — Bitcoin ecash protocol for privacy-preserving micropayments

- Fedimint — Federated Bitcoin custody and ecash

- BOLT 12 — Lightning offers specification

- FinTech Wrap Up — Is x402 the Stripe for AI Agents? (2026)

- Stripe Blog — Agentic Commerce Protocol announcement

- NIST AI RMF / CAISI RFI NIST-2025-0035 — AI Agent Standards (Jan 2026)